Biblioteca Comunale di Enna

Biblioteca Comunale di Enna Net Profit Margin: Definition, Formula, and How to Calculate

Data:

10 Febbraio 2022

The net profit margin formula may approximate the efficiency of this process. There are many different metrics that analysts and investors can use to help them determine whether a company is financially sound. One of these is the profit margin, which measures the company’s profit as a percentage of its sales. In simple terms, a company’s profit margin is the total number of cents per dollar that a company receives from a sale that it can keep as a profit. For example, if a company’s net income component percentage is 50 percent, it means that 50 percent of its total sales goes toward the company’s profits.

What Is a Common Size Income Statement?

Businesses and individuals around the globe perform economic activities with the aim of making a profit. Numbers like $X million in gross sales or $Y million in earnings are useful but don’t address a business’s profitability and comparative performance. Once you know a company’s net income and revenue, plug them into the equation above to find the net profit margin. That implies that 30 percent of the company’s revenues go toward its profits, while 70 percent goes towards its expenses. Founded in 1993, The Motley Fool is a financial services company dedicated to making the world smarter, happier, and richer. To see whether a business is constantly improving its profitability or not, the analyst should compare the ratio with the previous years’ ratio, the industry’s average and the budgeted net profit ratio.

How Can a Company Improve Its Net Profit Margin?

As a measure of profitability, the net profit margin is more complete because it accounts for all business expenses, not just COGS. Additionally, net profit margin can be misleading dollar-value lifo method calculation if a company decides to boost profits in the short term by reducing long-term expenses. As a result, net profit margin may look high, but only for a relatively brief period of time.

or Return on sales

However, like any other financial measurement, the net profit margin alone should not be the only metric used to assess a company’s financial health. For instance, a number that is considered strong in one industry may be considered low in another. This formula expresses the net income as a percentage of total revenue, providing a measure of the company’s profitability. In summary, ABC company’s profit margin is 35%, and its gross profit margin is 60%. Before you can evaluate the net profit margin, you’ll have to understand that it includes net profit and net sales. The net profit is defined by eliminating all of your expenses from your revenues, including wages, salaries, utilities, and many fees.

- The common size percentages can be subsequently compared to those of competitors to determine how the company is performing relative to the industry.

- Unlike these indexes, the net profit margin compares net income to total revenue.

- As a result, the company has greater depreciation expenses, reducing net income despite the impressive cash flow.

- For example, if your business generally has a 10% net profit margin and has a 12% margin this month, you can infer that you did a good job of controlling costs.

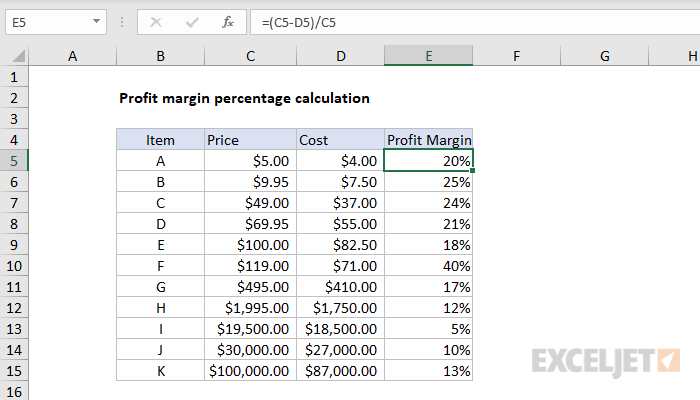

Your net profit margin displays the percentage of your sales is actual profit. This is after factoring in your cost of goods sold, operating costs, and taxes. To calculate your net profit margin, you just need to split your net income by your total sales revenue. Gross profit measures a company’s total sales revenue minus the total cost of goods sold (or services performed). Net profit margin also subtracts other expenses, including overhead, debt repayment, and taxes. The common size version of this income statement divides each line item by revenue, or $100,000.

As net profit margin is a ratio, so it may be known as either a decimal or a percentage. You just need to multiply the decimal by 100 to change it into a percent. The result you have is your net profit margin; just multiply this number by 100 to get a percentage.

Sales revenue measures the income brought in by the company’s core business activities. But while the definition may be straightforward, calculating sales revenue requires some more thought. Once you employ the net profit margin formula, it’s quite easy to compare its values over time and see what’s a company’s performance against the market or its main competitors. Gross profit margin and net profit margin are both profitability ratios that analyze different aspects of a company’s business. Gross profit margin accounts for COGS, while net profit margin accounts for all business expenses.

SG&A can include rent, utilities, marketing and advertising, salaries, and other operating costs. Gross sales revenue is the total of all sales of goods and services without taking into account any returns, discounts, or allowances. This figure indicates a business’ ability to sell its products or services.

Generally speaking, the gross profit margin reveals the profitability of specific items, while net profit margin is more focused on the bigger picture of running the business. To interpret whether a net profit margin figure is strong or poor, it’s helpful to compare it to peers or industry averages. The net profit margin can be calculated using the net profit and the revenue of a company, both of which are found on the income statement. For reference, it’s useful to know what all goes into the net profit figure.

In the Financial Manager, this ratio indicates the reported net income after taxes and other expenses in relation to the revenue from sales. Producers of luxury goods and high-end accessories can have a high profit potential despite low sales volume, compared with the makers of lower-end goods. A very costly item, like a high-end car, may not even be manufactured until the customer has ordered it, making it a low-expense process for the maker, without much operational overhead. Since they belong to different sectors, a blind comparison based solely on profit margins would be inappropriate.

Plus, net profit margin as a percentage makes it easy to compare the profitability of two or more companies. If there is a decline in the net income component percentage from the previous year to the current year, it means the company was not as profitable in the current year and may have even had a net loss. Common size income statements with easy-to-read percentages allow for more consistent and comparable financial statement analysis over time and between competitors.

Ultimo aggiornamento

11 Novembre 2024, 19:49